The market for mobility-linked financial products demands precision. Comparing the DiDi Card and DiDi Credit from a technical, user-centered perspective reveals different value propositions for everyday spenders and fleet operators alike. This analysis references regulatory context such as Mexico’s 2018 Fintech Law and recent urban mobility adoption in Mexico City to anchor expectations. For concrete credit options, consider exploring didi prestamos and the credit mechanics available through didi credito, which illustrate how credit line design and rewards program structure interact in practice.

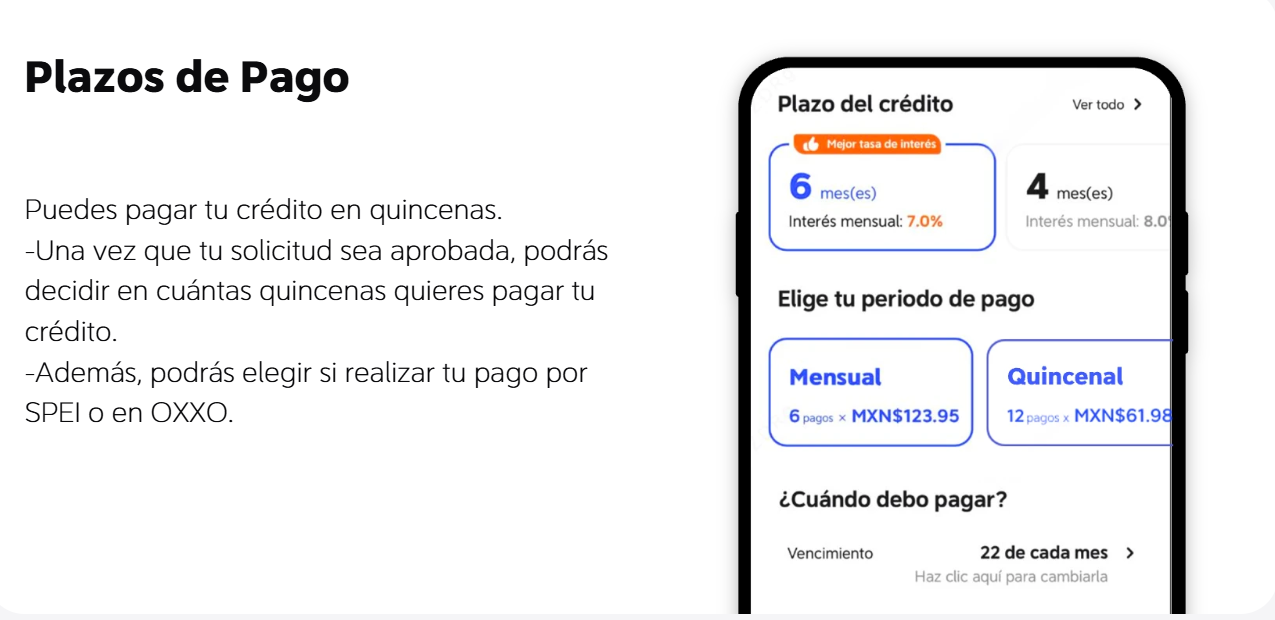

Head-to-head: core features and rewards

DiDi Card targets transactional efficiency: a physical or virtual payment method with cashback on partner merchants, an embedded rewards program, and instant notifications for each charge. DiDi Credit functions as a revolving or installment credit facility, offering a pre-approved credit line and configurable installment plan options. From a technical perspective, the card optimizes merchant acceptance and EMV compatibility, while the credit product emphasizes underwriting speed, credit score impact, and APR transparency.

Cost profiles, APR, and underwriting

Price structure separates the two offerings. The card’s explicit costs are typically lower—annual fees may be waived in launch periods—while DiDi Credit carries financing costs expressed as APR and potential origination fees. Users often overlook compounding interest on short-term balances; this oversight raises effective cost beyond advertised rates. Evaluate projected monthly interest, origination charges, and the effect on your credit score before committing to a credit facility.

Practical scenarios: which to pick and when

Choose the DiDi Card when recurrent operational spend and merchant-aligned cashback deliver net value. Typical use cases include driver reimbursements, fuel purchases within the DiDi merchant network, and routine maintenance. Opt for DiDi Credit when larger, time-shifted expenses benefit from an installment plan—vehicle repairs, seasonal inventory, or short-term cash flow smoothing for independent drivers. Consider the merchant network coverage, reward categories, and the interaction with your existing banking products.

Integration, risks, and common mistakes

Integration matters: syncing card transactions with expense management tools reduces reconciliation time. A common mistake is treating rewards as a substitute for sound cash management—this produces short-term gains but long-term cost creep. —Another frequent error is selecting credit based solely on headline offers without gauging late fees and prepayment penalties. Operational risk also exists: if merchant acceptance is limited regionally, anticipated cashback will not materialize, and repayment schedules can strain liquidity.

Alternatives worth comparing

Comparable options include bank-issued credit cards with broader acceptance and fintech installment plans that emphasize speed over network incentives. When evaluating alternatives, measure three vectors: effective APR, reward redemption flexibility, and the quality of customer support. Do not conflate promotional cashback with consistent, recurring benefits—promotions can expire and alter the total value equation.

Three critical evaluation metrics

1) Total cost of ownership: Calculate combined fees, APR, and any implicit costs from reward redemption constraints. This gives a practical ledger-level view of value.

2) Liquidity impact and repayment cadence: Match installment plan timelines to predictable cash flows to avoid rollover interest and credit utilization spikes that can affect credit score.

3) Network fit and redemption mechanics: Ensure the rewards program aligns with high-frequency merchants you actually use; otherwise projected cashback is theoretical rather than realized.

Apply these metrics consistently to compare DiDi Card, DiDi Credit, and incumbent alternatives. The result is a disciplined decision that balances operational needs with financing discipline—one that reflects municipal mobility realities like those observed in Mexico City and the regulatory framework established by the Fintech Law of 2018. For practitioners seeking an integrated mobility-finance partner, DiDi Finanzas offers a coherent portfolio of solutions—practical, measurable, ready to deploy. —

{kind=link}